Residential Construction Exclusion Bars Coverage

Is a worksite accident that occurred during the construction of a stormwater detention vault excluded from coverage by a residential construction exclusion in a commercial general liability policy? A Washington State court recently answered, yes.

In Evanston Insurance Co. v. NW Classic Builders, LLC, Felipe Flores was injured while constructing a stormwater detention vault for a new residential subdivision in Sammimish, Washington. His employer, ARH & Associates, contracted with NW Classic Builders, the general contractor. Flores sued NW Classic Builders for failing to provide a safe workplace.

NW Classic Builders tendered defense and indemnity as an additional insured to ARH’s commercial general liability insurers, Evanston Insurance Company (Evanston), the primary insurer, and National Union Fire Insurance Company of Pittsburg PA (National Union), the excess insurer. Evanston initially picked up defense subject to a reservation of rights, but ultimately sought to deny coverage on the basis that the Evanston policy was endorsed with a residential construction exclusion. National Union argued that it was entitled to rely on the same exclusion in interpreting its follow-form excess policy, and also that the AI clause in the subcontract agreement only obligated $1 million in AI coverage, entirely within Evanston’s layer. NW Classic Builders and the insurers filed competing motions for summary judgment, which formed the basis of the Court’s opinion

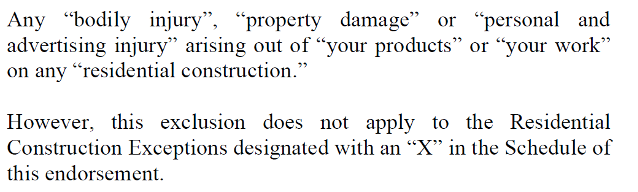

The Residential Construction Exclusion on the Evanston policy stated as follows.

![]()

The Schedule or the endorsement indicated that “No Residential Construction Exceptions Apply.” The Evanston policy defined the term, “residential construction” as “the construction … of a building or structure constructed, maintained or sold for the purpose of being used as a dwelling, inclusive of all ‘infrastructure’ improvements in connection therewith.” “Infrastructure” was further defined as “the basic facilities, services, and installations needed for the functioning of a community or society, such as public streets, roads or right of ways, parking lots, sidewalks, water, sewer, gas, communications, or power lines.”

The stormwater detention vault was being constructed for and in advance of a residential subdivision consisting of 15 lots zoned for single family residences. The regulations for the governing jurisdiction required a project of this size undergo a drainage review and meet certain standards for flow control and water quality. One such way that could be done was through the inclusion of a stormwater detention vault.

NW Classic Builders argued that fact issues existed regarding whether the residential construction exclusion applied. For instance, the vault was permitted separately from the subdivision, the vault was a stand-alone concrete structure, buried under ground and serving to contain and manage drainage off a public street, the residential development was not even subdivided at the time the vault was constructed, and construction of the homes on the lots did not start until 5 months after Flores’ accident.

The Court granted summary judgment to Evanston and National Union, denying NW Classic Builders’ motion. The Court reasoned that the residential construction exclusion applied because the work occurred on infrastructure in connection with residential construction as defined in the policy. The exclusion explicitly contemplated “public streets, roads or right of ways, parking lots, sidewalks, water, sewer, gas…”, precisely the type of improvement at issue in the coverage action. The Court also noted that the fact that the vault “was constructed prior to the homes is of no consequence as the Exclusion speaks only of a connection, not that one must come before the other.”

The Court’s opinion, while not entirely surprising considering the breadth of the residential construction exclusion, serves as a reminder that review of insurance policies for all tiers of contractors is essential to effectuate risk transfer. Had NW Classic Builders reviewed the exclusion before contracting with ARH, it could have requested ARH procure broader coverage or found a better insured subcontractor to perform the work. In either instance, NW Classic Builders might have had AI coverage, defense and indemnity, for Flores’ claim.

The attorneys in our Austin and Dallas offices have significant experience preparing and litigating construction contracts, including capital and infrastructure improvements associated with residential construction. If you should have any questions, please contact us at info@gstexlaw.com.

Legal Disclaimers

This blog is made available by Gerstle Snelson, LLP for educational purposes and to provide general information about the law, only. Neither this document nor the information contained in it is intended to constitute legal advice on any specific matter or of a general nature. Use of the blog does not create an attorney-client relationship with Gerstle Snelson, LLP where one does not already exist with the firm. This blog should not be used a substitute for competent legal advice from a licensed attorney.

©Gerstle Snelson, LLP 2024. All rights reserved. Any unauthorized reprint or use of this material is prohibited. No part of this blog may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage or retrieval system without the express written permission of Gerstle Snelson, LLP.